The Compression

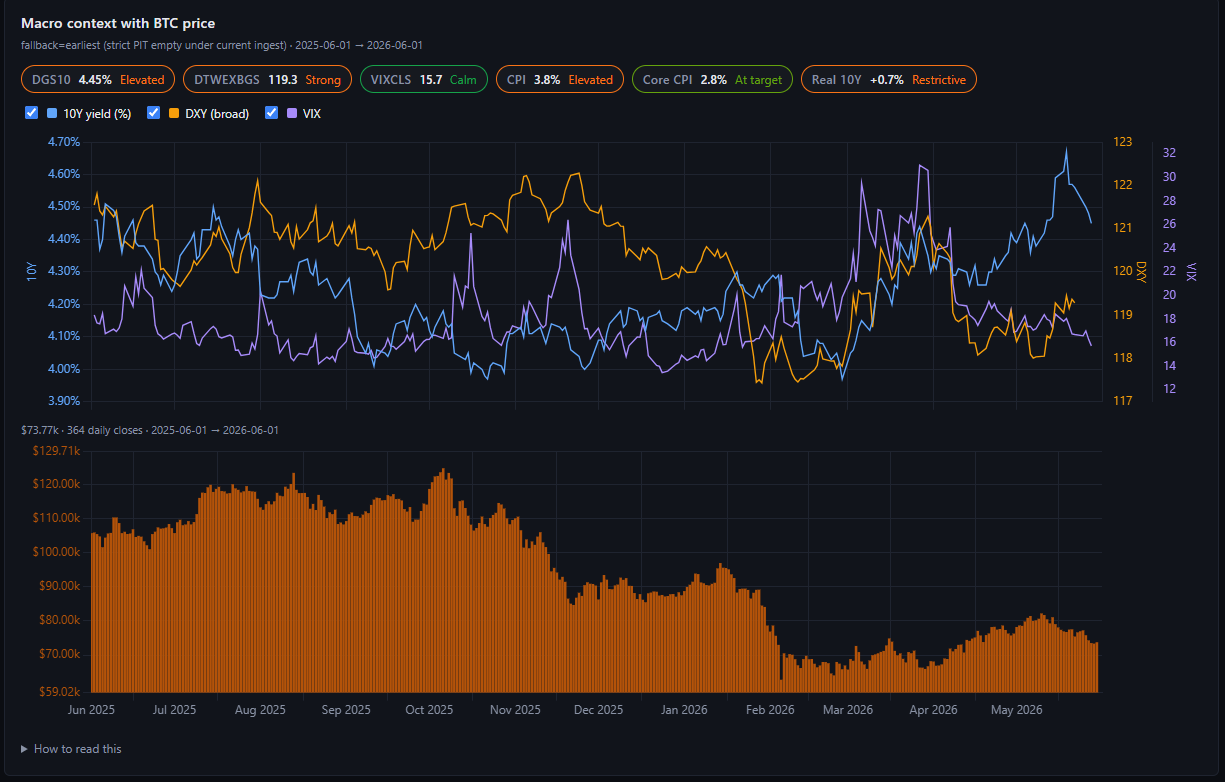

Bitcoin holds $73,771 inside a 700-point band.

Treasury yields hit their highest since 2007. Strategy bought bonds, not Bitcoin. Three mechanisms — ETF flows, the STRC funding apparatus, and the macro ceiling — are all pointing the same direction.

The compression began before most people noticed it. Bitcoin did not crash this week. It did not break. It simply stopped going anywhere, and the mechanisms that had been delivering it upward went quiet at the same time.

BTC opens the week of June 1 at $73,771. The range that has defined the past several sessions runs from $73,197 to $73,941. That is a 744-point band. Narrow enough to be called a ceiling and a floor simultaneously. The 7-day predicted close from the Hashpoint model is $74,917. A 1.55% lift. Not an escape. A holding pattern.

The power-law model has a 30-day target of $79,329 and a 90-day target of $92,298. Those numbers have not changed. The structural trajectory is intact. What has changed is the set of mechanisms available to deliver Bitcoin toward those numbers in the near term. They are all, at this moment, impaired.

This issue is about that impairment — what caused it, what it consists of, and what conditions would change it.

The first mechanism: the macro ceiling moved

On May 20, the 30-year U.S. Treasury yield hit 5.197%. That is the highest print since July 2007. Nearly two decades. The 10-year yield held near 4.44%, still elevated by any reasonable historical standard. The market response to these numbers was immediate: Bitcoin dropped 4–6% within a 24-hour window, accompanied by approximately $100 million in liquidations of leveraged long positions.

This is the mechanism through which bond yields constrain Bitcoin. Not through sentiment. Through opportunity cost. When the 30-year Treasury yields 5.197%, risk-free capital has an option it did not have when yields were near zero. Bitcoin, which yields nothing, must compete with that option in every allocation decision made by institutional capital. The higher the yield, the higher the implied hurdle rate for holding a non-yielding asset.

The VIX closed Friday at 15.32. Equity volatility is contained. That matters because it separates the current environment from a crisis configuration. This is not panic. It is repricing. Capital is not fleeing to safety — it is choosing yield over speculation. Those are different problems with different solutions.

The 10-year yield is the number to watch in the week ahead. A sustained move toward 4.25% or below would begin to relieve the macro ceiling. A move toward 4.7% or higher would press the $73,197 floor.

The second mechanism: Strategy stopped buying

On May 24, Michael Saylor posted four words that defined the week for anyone watching the institutional demand picture: "bought bonds, not bitcoin." The BitVac, as Saylor termed it, was charging. Preparing for the next acquisition cycle, not executing one.

The context matters. Strategy is repurchasing approximately $1.5 billion in convertible senior notes due 2029 at a discount. This is liability management: retiring debt cheaply ahead of future Bitcoin accumulation. It is not a retreat from the Bitcoin thesis. But in the near term, the practical effect is the same as any other pause: the largest single institutional bid in the Bitcoin market was absent for the week.

This is the third pause in Strategy's weekly buying cadence in 2026. The prior two resolved quickly, with Saylor's "back to work" posts signaling resumption within days. The BitVac framing suggests the same pattern here. But until the next purchase disclosure arrives, the bid is silent.

STRC sits at $98.99. Still below the $100 par anchor, still 101 basis points from triggering the at-the-market program. The ATM program remains closed. The funding mechanism for the world's largest corporate Bitcoin accumulator has now been effectively suspended for most of the past three weeks.

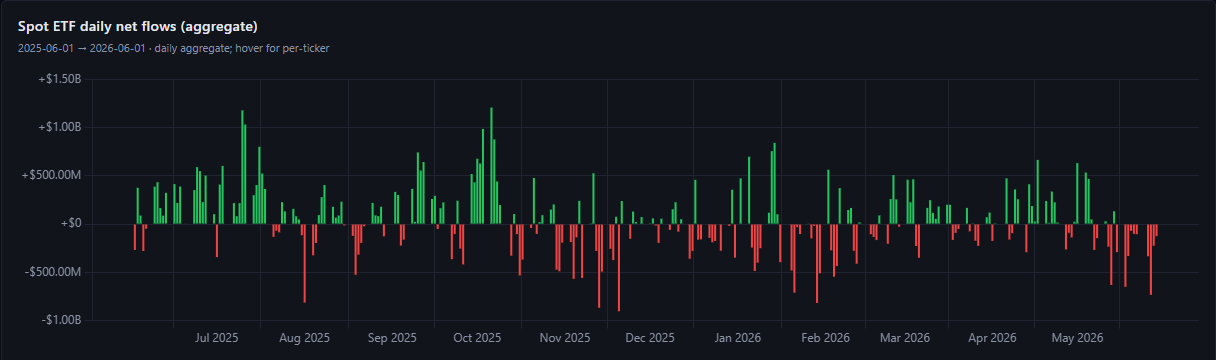

The third mechanism: ETF flows turned sharply negative

Six consecutive days of outflows. That is the ETF flow picture entering the week of June 1. The week of May 26 alone produced $1.42 billion in net outflows from U.S. spot Bitcoin ETFs. May 27 and May 28 together saw $897 million in long liquidations alongside the ETF exits. The year-to-date net inflow figure for 2026 has shrunk to $536 million — a fraction of what it was at the April high-water mark.

The composition of the outflows is significant. IBIT and FBTC together account for more than 74% of the week's exit. That is not retail. That is large institutional allocators reducing exposure in a coordinated fashion. The catalyst, according to market analysts, was the combination of U.S. airstrikes near the Strait of Hormuz, Bitcoin falling below $73,000, and a general decline in risk appetite tied to the Treasury yield picture.

There is a structural counterpoint worth noting. ETF AUM as a percentage of total Bitcoin market capitalization has climbed to 7.16%. The ownership base is deepening even as nominal dollar flows are negative. The long-term structural holder base is larger than it has ever been. The short-term flow picture is noisy.

What the structural read says

Three mechanisms, three impairments, one compression band. Bitcoin is not in a bear market. The power-law envelope holds. The post-halving cycle is intact. The Hashpoint model's 90-day target of $92,298 and 1-year target of $197,199 are unchanged. The cycle position sits in a range that, across prior post-halving periods, has generally preceded rather than followed the bulk of the cycle's price appreciation.

What is constrained is the near-term delivery mechanism. The macro ceiling is elevated real yields. The institutional bid is paused at two levels simultaneously — Strategy and ETFs. The compression band is the result.

The compression will resolve. The question the structural read asks is not whether it resolves, but which of the three mechanisms resolves first, and in which direction.

Hashpoint Magazine publishes a structural reading of Bitcoin's current state. We are not predicting prices. We are not making investment recommendations. We are reading the mechanisms that connect institutional capital, regulatory progression, and price formation, and surfacing what those mechanisms say about where Bitcoin sits in its long-run envelope. Decisions about positioning, exposure, and timing are yours alone.