The CPI Print That Broke the Rally

April inflation data forced Fed funds futures to reprice from rate cuts toward rate hikes. The macro environment for Bitcoin is now restrictive, not accommodative.

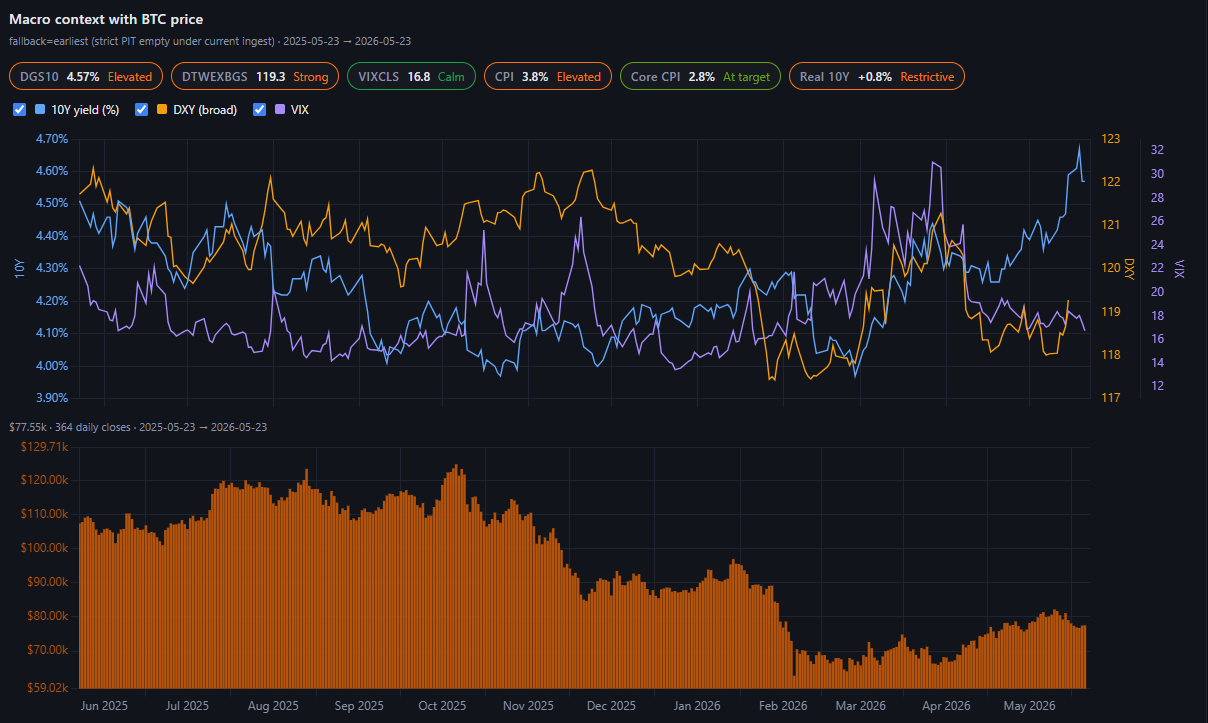

Bitcoin does not trade in a macroeconomic vacuum. The dashboard's macro panel exists to make that explicit. This week, the most important entry in that panel changed character.

The April CPI release printed at 3.8% on the headline measure, with core CPI at 2.8% and the Producer Price Index jumping to 6%. The headline figure is the highest since September 2023. The Federal Reserve has now missed its 2% inflation target for five consecutive years.

The market response was not subtle. Fed funds futures repriced almost immediately from a base case of modest rate cuts through 2026 to a base case that includes a 60% probability of at least one rate hike by year-end. This is not a marginal adjustment. It is a wholesale shift in the macro setup, the kind that reprices risk assets across categories simultaneously.

Why the real yield number matters more than the headline

The dashboard's macro panel shows the nominal ten-year Treasury yield at 4.57% and the real ten-year yield, adjusted for inflation expectations, at +0.8%. The label on that reading is "Restrictive," and the label is accurate.

The mechanism through which real yields affect Bitcoin is not intuitive to everyone, so it is worth stating plainly. Bitcoin produces no yield. It pays no dividend, no coupon, no interest. Its value is a function of what investors believe it will be worth in the future relative to the alternatives they give up today. When real yields are negative or near zero, the opportunity cost of holding a non-yielding asset is low. When real yields are positive and rising, the opportunity cost increases. Capital has a better offer.

This is the macro environment that persisted through most of 2022 and into 2023, when the Fed was hiking aggressively and Bitcoin fell from $68,000 to under $16,000. The environment that followed, declining real yields, rate-cut expectations, accommodative posture, was a significant contributor to the recovery cycle that has since carried Bitcoin into the $75,000-$95,000 range.

The April CPI print has not recreated 2022. But it has materially altered the directional expectation. The market is no longer pricing a path toward lower real yields. It is pricing a path toward higher ones.

The PPI signal and what it implies

The Producer Price Index reading of 6% is, in some respects, the more alarming number. PPI measures the cost of goods at the producer level before they reach consumers. It is widely regarded as a leading indicator for CPI: when producers are paying more, consumers typically follow. A 6% PPI reading with CPI already at 3.8% suggests the inflation the CPI is measuring has upstream supply-chain reinforcement. It is not simply a statistical artifact of base effects.

For the Fed, this complicates the calculus considerably. Rate cuts require confidence that inflation is moving durably toward 2%. A 6% PPI reading, combined with the highest CPI since September 2023, does not provide that confidence. Five consecutive years of missed inflation targets make the politics of cutting rates fraught. The Fed has institutional credibility concerns that make it slow to ease in the face of data like this.

What the dashboard's macro panel is actually measuring

The panel tracks five macro variables: the nominal ten-year yield (DGS10), the real ten-year yield, CPI, the VIX, and the DXY dollar index. Each is labeled with a qualitative assessment, Elevated, Restrictive, Calm, Strong, calibrated to Bitcoin's historical sensitivity to each variable.

The current configuration is uniformly cautionary. DGS10 at 4.57% is Elevated. Real yield at +0.8% is Restrictive. CPI at 3.8% is Elevated. The only relief in the panel is the VIX at 18, which remains in Calm territory. The equity market has not yet registered the macro repricing as a crisis signal.

That VIX reading is worth watching. Historically, the combination of elevated real yields and rising rate-hike expectations eventually transmits to equity volatility. If the VIX moves from 18 toward 25, the macro configuration for Bitcoin worsens on two fronts simultaneously: real yields remain restrictive, and risk-asset correlations tighten, pulling Bitcoin downward alongside equities.

The structural read

The macro headwind created by the April CPI print is real, and it is the most durable of the three mechanisms examined in this issue. ETF flows can reverse in a week. STRC can recover above par in a week. The macro environment reprices on a slower cycle. The next CPI print arrives in mid-June, and there will not be a Fed meeting until later that month. The restrictive macro configuration will persist as the backdrop for Bitcoin's price action through the remainder of May.

What we monitor in the week of May 25 is whether the PPI signal translates into another upside CPI surprise in June, or whether the April print represents a peak rather than a trend. The former would deepen the restrictive configuration. The latter would begin to relieve it.

For now, the macro panel reads as a headwind, not a tailwind. That is the honest structural reading, and it is the one worth carrying into the week ahead.