Three Pillars, One Crack: How Bitcoin's Spring Rally Met the Mid-May Pipeline

Spot ETF flows reversed, Strategy's funding mechanism breached par, and a single CPI print forced a wholesale repricing of Fed expectations. All in one week. All compounding.

The thesis of Bitcoin's spring rally was simple and widely held. Institutional demand had finally arrived in durable form. Spot ETF inflows had run positive for six consecutive weeks through early May. Strategy, the corporate accumulator that dominates the non-ETF channel, was buying aggressively, funded by a preferred-stock instrument that had achieved a kind of mechanical stability. The macro picture, while not benign, was no longer actively hostile. The Digital Asset Market Clarity Act had cleared its Senate Banking Committee hurdle on May 14, advancing toward a framework that institutional capital had been waiting on for years.

Each of these was a real development. None of them was illusory. And yet in the second week of May, Bitcoin's price compressed downward against all of them simultaneously. The dashboard at Bitcoin Hashpoint registered the events in real time: cycle position fell from above 0.20 to 0.15 in eight trading days. The structural envelope did not break. But something cracked underneath it.

What broke was not the bull case. What broke was the demand pipeline that had been delivering the bull case to spot price.

This issue is about that crack, the three mechanisms that produced it, and what the structural read of Bitcoin's current state actually says. Not what the headline narrative says. What the mechanisms say.

The first pillar: ETF demand reversed in concert

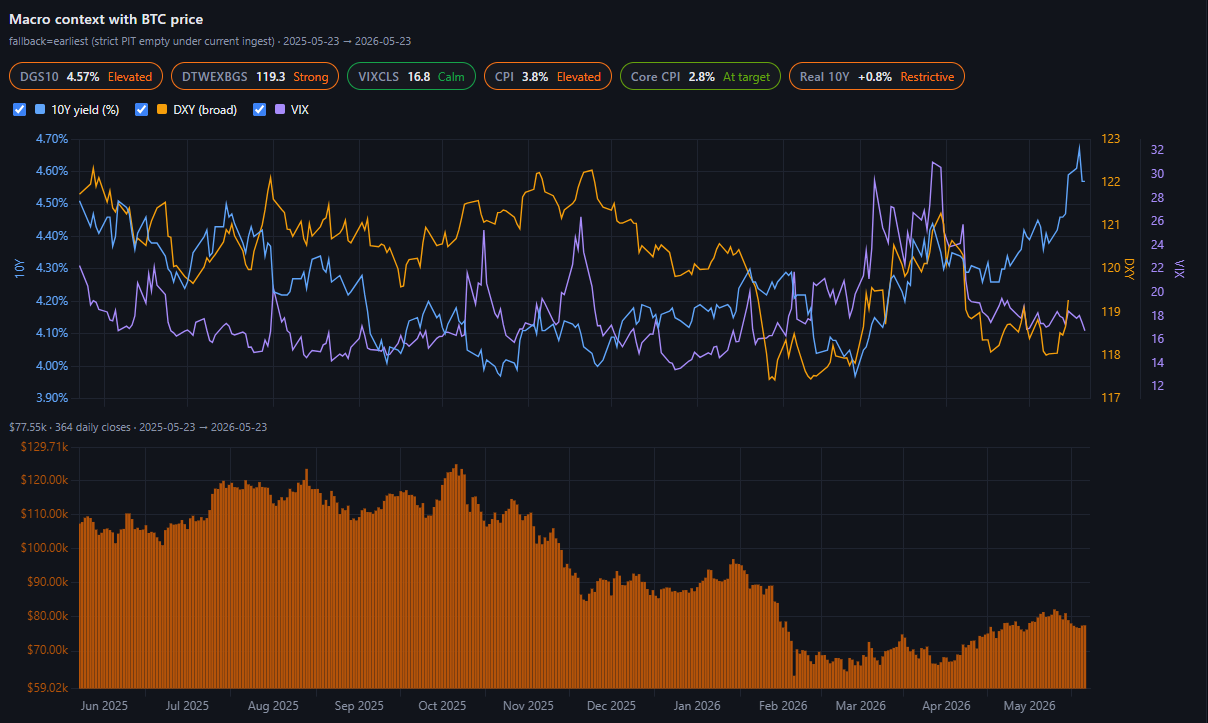

Through the first week of May, U.S. spot Bitcoin ETFs were a quiet, dependable absorber of supply. The May 1 trading session alone produced $629 million in net inflows. Cumulative inflows since launch in early 2024 had crossed $58 billion. The category had become institutional infrastructure: a regulated, custodied, fee-bearing access point that traditional capital could use without operational friction.

Then it stopped.

The week ending May 15 produced a net $1 billion outflow across the eleven U.S. spot Bitcoin ETFs. May 13 alone saw $635 million of outflows in a single trading session, the largest single-day net outflow since late January. The following week was no better. CoinShares reported the largest weekly outflow of 2026 across all digital asset investment products, with Bitcoin products responsible for nearly all of it.

The mainstream framing cited Iran-related geopolitical risk and elevated oil prices. Both were real. Neither alone is sufficient to explain a $1 billion-plus reversal across a category that had been net-positive for six weeks running. What the flow data shows, more honestly, is that the demand was reactive rather than committed. The inflows of late April and early May had been positioned for a continuation of the rally. When the rally stalled, the same capital reversed.

This matters for the structural read because it tells us something durable about ETF demand in 2026: it amplifies trends but does not create them. ETFs are the most-watched indicator and the most institutionally legitimate channel, but their flows follow rather than lead. Treating ETF flows as a leading signal, as much of the commentary does, has the causality backward.

The second pillar: Strategy's funding mechanism breached par

The second pillar is more mechanically significant and less widely understood.

Strategy, the corporate entity formerly known as MicroStrategy, has been the dominant non-ETF buyer in 2026. The company holds 843,738 BTC as of its most recent SEC filing, acquired for roughly $63.9 billion. The average cost basis is $75,700 per coin. To fund continued accumulation, Strategy has built a capital-markets apparatus consisting of common stock issuance, debt instruments, and most importantly a perpetual preferred stock called STRC.

STRC pays an 11.50% annual dividend, adjusted monthly, with the explicit mechanical goal of trading near its $100 par value. When STRC trades at or above par, Strategy aggressively issues new shares through an at-the-market program, raising capital that flows directly into Bitcoin purchases. When STRC trades below par, the company is structurally constrained from issuing. Doing so at a discount would dilute existing holders and damage the funding mechanism.

The week of May 11-17, Strategy raised $2.01 billion through STRC issuance and purchased 24,869 BTC at an average price of $80,985. This was the largest single weekly accumulation in months. By Strategy's own internal standard, it was executed at attractive prices relative to their average cost basis.

Then STRC slipped below par.

The dashboard's STRC card has shown the at-the-market program as CLOSED for most of the past week. STRC has traded around $99.30, a 0.70-point gap below the $100 anchor. The company is now in a defensive posture with respect to the funding mechanism, not an offensive one.

The mechanical implication is direct. As long as STRC trades below par, the largest non-ETF supply absorber in the Bitcoin market is structurally suspended. The next test arrives May 28: if STRC trades at or below 99.49 on a volume-weighted basis from May 1 through May 28, Strategy is contractually required to raise the dividend rate by 25 basis points to 11.75%. The economic consequence is that financing costs increase, which compresses the rate at which new Bitcoin can be accumulated without diluting per-share holdings.

This is the most underappreciated mechanism in current Bitcoin price action. Strategy's bid has been the single most reliable institutional demand source in 2026 by capital deployed: roughly $5.58 billion through STRC alone year-to-date. When that mechanism is suspended, the marginal-buyer picture thins considerably.

The third pillar: the CPI print broke the macro setup

The macro environment had not been benign through 2026, but it had been navigable. Real ten-year yields were positive but not extreme. The Fed was in a holding pattern, with rate-cut expectations modest but present. The dollar index was strong but not breaking out. The VIX was calm.

Then the April CPI print arrived in mid-May.

Headline CPI came in at 3.8%, the highest reading since September 2023. Core CPI held at 2.8%. The Producer Price Index, often a forward indicator, jumped to 6%. The market response was immediate. Fed funds futures repriced a 60% probability of a rate hike by the end of 2026. That is a stark reversal from the prevailing expectation of modest cuts.

For Bitcoin, this repricing matters more than the absolute level of yields. The Fed cutting rates means real yields fall, which raises the relative attractiveness of non-yielding stores of value. The Fed hiking rates means real yields rise, which does the opposite. The market is no longer positioned for the first scenario; it is now positioned for the second. The current dashboard reading of +0.8% real ten-year yield is labeled "restrictive" for a reason. Capital that might have flowed toward Bitcoin gets a different option when real yields are positive and rising.

What the structural read actually says

The three pillars did not fail in sequence. They cracked in concert. The CPI print on May 13 was the proximate trigger. It forced the macro repricing, which triggered profit-taking that showed up as ETF outflows, which produced the price weakness that pushed STRC below par. The mechanisms are linked.

This is not a bull thesis breaking. The structural envelope holds. Bitcoin currently sits at a cycle position of 0.15, well above the power-law floor near $57,000 and far below the median near $136,000. The post-halving cycle is intact. Strategy still holds 843,738 BTC. Cumulative ETF inflows remain above $58 billion. Hashrate has recovered to over 1,000 EH/s, up 19% over the prior thirty days. That kind of hashrate recovery has historically preceded price recoveries, not followed them.

What broke is the marginal-buyer pipeline. The three mechanisms that had been delivering steady demand to spot prices in April and early May are now all in a constrained state simultaneously. ETF flows are reactive and currently risk-off. Strategy is suspended at the funding layer. The macro environment is restrictive rather than accommodative.

The current state is not bearish. It is constrained. Those are different things.

Bitcoin Hashpoint exists to read these mechanisms structurally rather than narratively. The narrative read of this week was simple: institutional sentiment has turned. The structural read is more useful. Three demand mechanisms hit friction at the same time, each for different but compounding reasons. The narrative implies a verdict. The structural read implies a set of specific conditions to monitor, each of which can resolve independently.

What we will watch for as the week of May 25 begins is whether any of these three mechanisms unsticks. STRC's recovery above par is the most consequential and the most monitorable. The next CPI print is two weeks out. ETF flow direction will be visible daily.

The publication's posture, here and going forward, is that we are watching the mechanisms, not the price. The price is the output. Understanding which mechanisms are working and which are constrained at any given moment is the analytical task. The headline number, in isolation, tells you nothing about that.

This issue exists to make those mechanisms visible. Each of the supporting articles below examines one of them in detail. The Hashpoint, our closing piece, translates the structural read into the simplest accessible terms.

Hashpoint Magazine publishes a structural reading of Bitcoin's current state. We are not predicting prices. We are not making investment recommendations. We are reading the mechanisms that connect institutional capital, regulatory progression, and price formation, and surfacing what those mechanisms say about where Bitcoin sits in its long-run envelope. Decisions about positioning, exposure, and timing are yours alone.